SilverDoor's Market Update is a comprehensive review of the global travel landscape using our own booking data, wider economic context, and our experts' experience and predictions to build a picture of serviced apartment trends worldwide. Reflecting on the past quarter and forecasting for the year ahead, the report advises corporates on rates, supply, demand and traveller preference to inform booking practices.

SilverDoor captures more than 127,000 datapoints from an average of 593,000 enquired room nights each quarter, the largest and most extensive sets of data available in the sector. This means we can provide the most accurate trend commentary and forecasting for those in the know across the business travel and mobility industry.

_______________________________

| SilverDoor Snapshot

Hiring freezes and cooling job markets; AI as the modern-day gold rush and the hardware production needed to support it; and against-the-odds record investment in offshore wind and energy projects – let’s dissect the corporate demand drivers of the moment.

_______________________________

| Demand Drivers: where are corporates going right now (or not)?

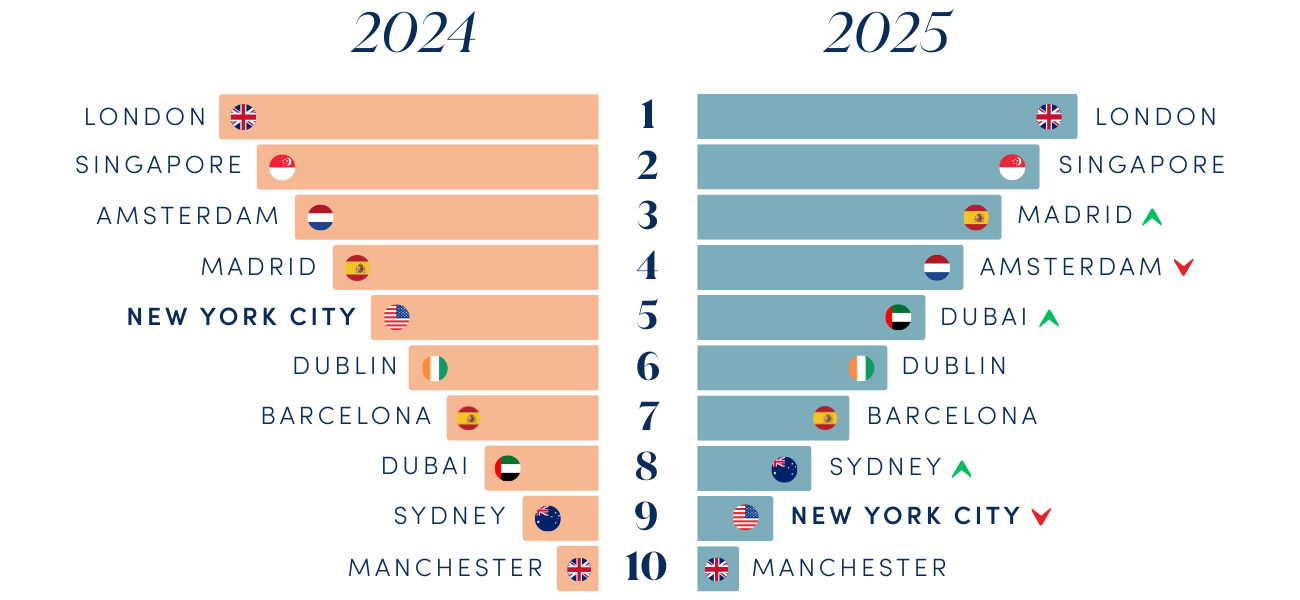

In the US, we’re seeing a decline in demand for New York City: NYC enquiries have dropped 29% for the first half of 2025 compared to the same period last year. It’s even been knocked down our top locations list and replaced by Dubai in our global top five – indeed Dubai bookings were up 65% YoY this quarter:

2024: London, Singapore, Amsterdam, Madrid, New York City

2025: London, Singapore, Madrid, Amsterdam, Dubai

Factors contributing to a decline in NYC demand this year include the continued challenges around short-term rentals and a weak employment market with “slowest job growth since 2003”. If businesses are hiring significantly less than they were last year, there’s fundamentally fewer people to move around, not to mention hiring freezes are usually part of an effort to cut costs – travel budgets might then be feeling the squeeze and causing a drop off in mobility.

The current NYC mayoral election campaign (scheduled for early November) might also be playing a part. The current frontrunner, Zohran Mamdani, wants to make changes to the city tax system if elected – like the influence of tariffs we reported last quarter, could the possibility of a new city government be inspiring some businesses to look into diversifying their operations elsewhere? History has shown that drastic changes to tax following an election result are unlikely, but it will be interesting to see if businesses seek to protect themselves from the risk of another divisive political change on the horizon.

Looking at average daily rates (ADR) for NYC, for the past quarter our booking data shows a 41% YoY increase, enquiries converting at $446 compared to $317 last year. Typically, low demand would mean falling rates as operators are more likely to go low to secure occupancy, but these high rates might be a cause rather than a symptom. The high costs of staying in New York compared to other US destinations are likely another deciding factor for corporates to go elsewhere.

If we then we look at our global top ten to examine New York City’s position in more detail, we can see it’s fallen to ninth place and been overtaken by Sydney:

2024: London, Singapore, Amsterdam, Madrid, New York City, Dublin, Barcelona, Dubai, Sydney, Manchester

2025: London, Singapore, Madrid, Amsterdam, Dubai, Dublin, Barcelona, Sydney, New York City, Manchester

This represents a 5% YoY increase in Sydney enquiries. In our customer base, this uptick in demand for Sydney has been driven by the professional services and banking sectors, and the Australian government’s investment in infrastructure and sustainable energy goes some way to explain the trend as consulting and engineering firms will be involved with these projects.

| If New York is quieter than usual, which US locations are picking up?

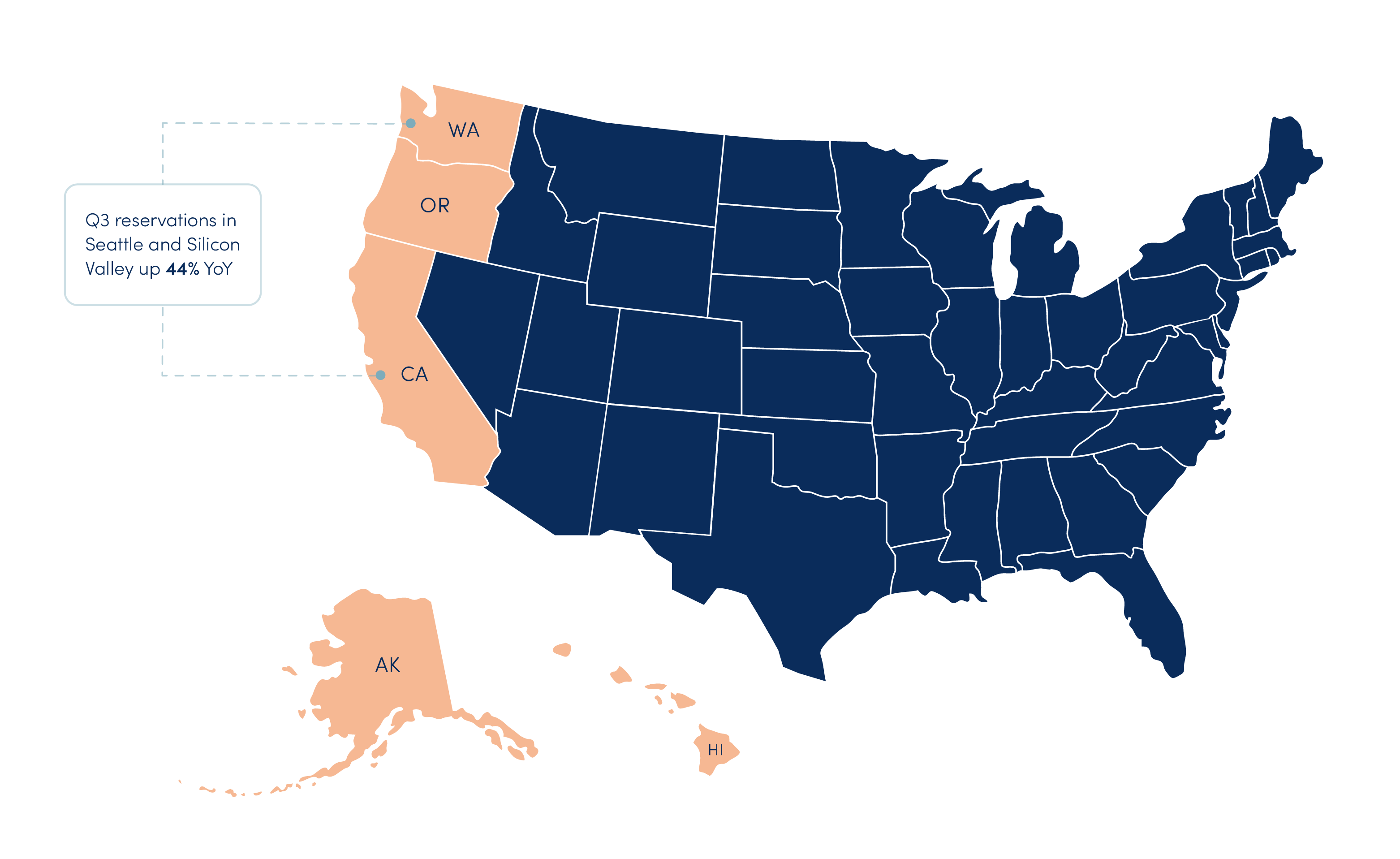

Our US account managers are reporting that NYC is being outpaced by strong corporate demand for corporate housing in West Coast states Washington and California, particularly in Seattle and Silicon Valley where Q3 combined reservations were up 44% YoY. Unsurprisingly it’s the tech scene luring both domestic and international visitors here, as the West Coast spearheads research, investment and development into AI and machine learning.

Whether it’s for conferences and industry events or project-based trips and relocations, tech sector mobility in the US West Coast is strong and not showing signs of slowing. From a supply chain perspective, our Acquisition Specialists report a 31% YoY increase in our stock in California State and a 45% YoY increase in Washington State, representative of this sustained demand.

This summer has seen several Washington city councils pass zoning and housing code amendments, which should help with more approved planning for corporate housing builds and further growth to the Washington supply. In June, the Californian Governor also finalised budgets which include advancing more housing and infrastructure by reforming long-standing development barriers. This investment aims to ease the affordability and accessibility of housing for locals, which could in turn ease the regulations around short-term rentals and speed up the approvals of new developments.

The business-friendly tax environment in Texas also made Dallas and Houston hotspots this quarter. Driven by the growing tech scene here, the relatively low operating costs and corporate tax rates make Texas attractive to businesses – it’s home to 54 Fortune 500 companies, topped only by California with 58. The relatively low living costs and personal tax rates also make it popular for employee relocations, with the state again second only to California in terms of tech workforce size.

These competitive advantages are nothing new, but with Q3 2025 bookings up 58% YoY in Houston, it does seem to have had a bit of a resurgence this summer. In terms of pricing in Houston, ADR for the quarter was $208.79, which represents a per-night savings opportunity of $237 compared to booking in NYC.

| What does a thriving tech scene in the US mean for the rest of the world?

As for availability, APAC account managers have reported challenges with supply not being able to keep pace with the demand levels in both Tokyo and Taiwan. It’s a double-edged sword in Tokyo, where ordinarily we’d suggest longer lead times to avoid missing out on options, but we’ve actually struggled to secure availability far in advance because properties typically offer extensions to in-house guests before offering availability for new enquiries.

To mitigate the impact of availability challenges in high-demand locations, corporates could consider staying outside of busy central hubs and widening your search to nearby commutable locations. Also, whilst availability can’t always be secured far in advance, engaging with suppliers early can still help to secure soft holds where possible and join cancellation waitlists.

These APAC trends come as the demand lull we reported in the last Update continues in Singapore. It’s still our top APAC city, but demand is 10% lower YoY. On the reverse of ADR trends in NYC, our booking data shows a symptomatic 13.5% YoY decrease in Singapore ADR as bookings converted for S$275.43 in the last quarter compared to S$318.44 in the same quarter last year.

Our APAC account managers have reported a softer market and more negotiation opportunity in Singapore compared to other locations, except for limited availability room categories like two- and three-bedroom apartments. Booking data for Q3 2025 does show a 40% YoY increase in ADR for the two- and three-bedroom category (converting at S$470.50 in Q3 2025), compared to a 6.5% YoY decrease for the studio and one-bedroom category (converting at S$256.67 in Q3 2025). If you’re travelling with your family and need a bigger space, you could consider interconnecting one-bedroom apartments to avoid the extra costs.

As NYC falls from our global top five, Dubai enters – with Dubai bookings up 65% YoY in Q3. This sustained demand for Dubai and the wider Middle East region is especially driven by extended stays and relocations for assignees in the financial, pharma and law sectors from companies expanding their operations in the region. With relocation bookings especially, our Gulf team have noted the importance of in-person viewings with the client to ensure the accommodation is what they’d want for a long stay.

In Spain, it’s the energy industry driving demand trends. Spain is a big player in European renewable energy production, with investment into projects to develop solar and wind output particularly on the rise. Our Iberia account managers are reporting more remote coastal requests near Valencia and Bilbao for project workers on offshore wind farms, and around Zaragoza for solar and green hydrogen plants.

For this past quarter, Bilbao bookings were up 50% compared to the same period in 2024 and up fivefold in Zaragoza. As for Valencia, the number of room nights booked was a huge 380% higher compared to 2024. This demand driver is indicative of global renewable energy investment for the first half of 2025 still beating 2024 records, despite fears about the worldwide influence of US sustainability policy amendments – BloombergNEF citing offshore wind and small-scale solar projects spurring 2025 investment growth so far.

Key Spanish business hubs have also been busy over the summer, with bookings doubling YoY in both Barcelona and Madrid this quarter, which are up 100% and 102% respectively, and Madrid has even replaced Amsterdam in our top three global locations last quarter. However, in Spain and across EMEA, – in both existing programmes and procurement exercises. Onboarded coverage numbers will always be important, but strong sourcing capability, particularly in tertiary or high-risk locations, will increasingly be a differentiator.

| TMC and RMC trends, and how current economic contexts are influencing the outlook for the rest of the year

From our travel management partners, we’ve been hearing about a shift in how corporate travellers are choosing serviced apartments. In the past, guests would look to their TMC to recommend the best accommodation options for their stay, but now more guests are making an enquiry with specific operators or properties in mind. This is a clear indicator that the serviced apartment/extended stay sector is continuing to mature, and that brands are building loyalty by delivering consistently positive experiences.

|

In a change throughout the sector, we’re also seeing more brands with a strong presence across multiple markets and guests actively seeking out their properties. For example, if a guest has a great experience staying in a London property operated by a particular serviced apartment brand, they’re more likely to a) book that property again for their next London visit, and b) book the same brand when they need to stay in Manchester. Guests trust in the consistent high levels of quality and service they’ll receive from serviced accommodation operators, so are increasingly loyal to the brands they know and love. Brand loyalty is typically associated with the hotel sector and its long-standing loyalty programmes, but does this represent further narrowing of the competitive gap between hotels and serviced apartments? |

We’ve also heard feedback to suggest that expense policies aren't always keeping pace with the lifestyle preferences of corporates staying in a serviced apartment. Subsistence budgets are often calculated per meal or per day, rather than per week or per trip. This works if you’re staying in a hotel and eating out for every meal, but if you’re staying in a serviced apartment for longer you might choose to do weekly grocery shops instead.

Preparing home-cooked food saves money and is more likely to result in healthier eating habits, but a per-meal budget allowance that limits (or even penalises) travellers preparing their own food doesn’t let businesses, or their assignees, reap the full benefits of choosing a serviced apartment. The Autumn issue of the Business Travel Magazine offers advice for managing F&B spend – including flexibility with the cost of living in different destinations – but the need for flexibility to buy groceries is still overlooked in many policies. Guidelines around subsistence allowances for corporate trips is certainly something we'd encourage businesses to think about.

On one hand, the impact of tariffs on stock prices might not have been as negative as the world was dreading, and it seems the lag of negative impact we mentioned in the last report – where lengthy approval lead times can mean there’s a delay in how market shifts affect relocation volumes – may not actually come to fruition. Indeed, bookings via RMCs were up 7% this quarter compared to the same period last year, indicating a sustained investment in mobility despite economic uncertainty.

Stronger relocation demand could also be explained by the current complexities of global travel making it more difficult for businesses to organise permanent transfers in-house, so they might instead be looking to RMC partners to support with challenges around visas, travel bans, cancelled flights, and shipment delays.

On the other hand, though, ongoing trade conversations and tariff pauses might still be making it difficult for businesses to confidently commit to projects or investments. This lack of confidence was impacting both direct corporate and TMC booking volumes, manifesting as a cautious first half of the year, but a stronger last quarter and positive predictions from many clients suggest a busy end to 2025.

_______________________________

_______________________________

If you would like specific topics or trends to be discussed in a future SilverDoor Market Update, get in touch with us at [email protected].