If corporate accommodation buyers and operators had a Christmas list, a crystal ball to predict pricing and demand would probably be near the top. Instead, gaze into SilverDoor’s Market Update for 2026 ADR forecasts and the top trends influencing global business travel right now.

In this report, buyers can see current and projected pricing trends in all global regions, and how major upcoming events are already shifting the annual outlook. Operators can understand how corporate pressure and demand are shaping up, and find out the key growth opportunities to plan for.

This Market Update has all the intel you need to get ahead for 2026.

_______________________________

SilverDoor Snapshot

Global average daily rates are rising. Lead time and average length of stay are shortening across the board. Demand is strong, and housing solutions are diversifying to meet an evolving sector.

Our last Market Update of 2025 analyses global pricing, demand and availability trends to build a picture of where the corporate accommodation, business travel and mobility sectors are heading into the New Year.

_______________________________

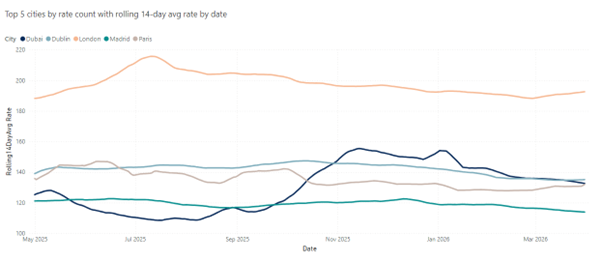

EMEA Booking Data Trends

- Average daily rates (ADRs) in EMEA markets like London, Dublin and Paris are currently forecasted to see YoY increases of up to 11% by the end of April 2026.

- The Milano Cortina Winter Olympics in February are pushing rates in Milan up to 49% higher YoY.

- The average length of stay (ALOS) for one-bedroom reservations in EMEA last quarter was 42 nights: 4 nights (9%) shorter YoY.

Slightly shorter stays are more normal during this period when there’s more travel for conferences and trade fairs, and is indicative of increased serviced apartment usage for short-term business travel. - The average lead time for one-bedroom enquiries in EMEA last quarter was 39 days: 8 nights (17%) shorter YoY.

Our relocation and global mobility clients have advised us that approvals for new initiations are taking longer than usual at the moment due to delays with visa and immigration processes, which will be bringing down average lead times across the region.

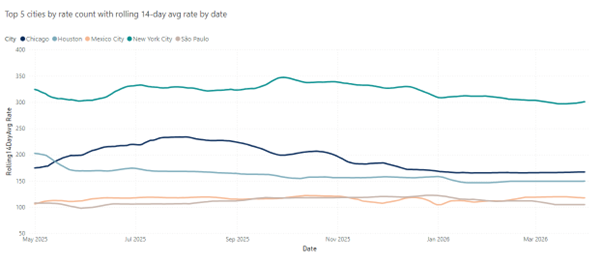

The ADR forecast in key EMEA cities

Dubai ADR peaks earlier in the year, while many European markets are higher around June-August

In London, one-bedroom ADR is expected to be £191 by the end of January 2026 but is predicted to climb above £202 by mid-June when we’d typically expect peak season prices like we saw this summer. Our 2026 booking data is currently predicting London ADR to increase by at least 8% YoY by November 2026.

Dubai’s downward trajectory over the next quarter will continue as it comes out of its peak season: after ADR highs of AED 745 in January (influenced by strong demand and supplement charges over Christmas and New Year), the trend will continue to decline until ADR begins to peak again come September.

The Paris market has corrected post-Olympics, with average pricing coming down as much as 18% since peak event demand in July/August last year. ADR in both Dublin and Paris is expected to dip slightly around February/March before beginning an upward trajectory into the spring and summer. Dublin ADR is forecast to reach €176 by October 2026 (7% YoY increase), and Paris ADR is predicted to reach €162 by the same time (8% YoY increase).

Outside of these central business zones, there’s a continued need for tertiary locations. In the UK alone, bookings into tertiary locations increased by 6.5% YoY in the past 12 months, as corporate guests are increasingly those travelling for construction, engineering, infrastructure, manufacturing or civil service projects, and more commonly aren’t exclusively heading to the big cities.

|

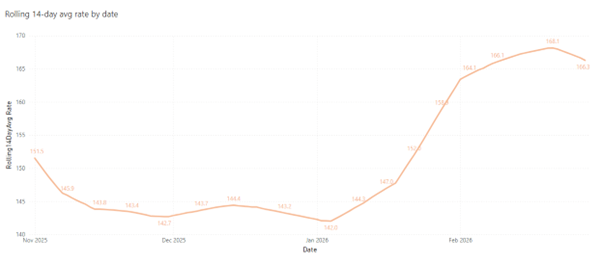

The Milano Cortina Winter Olympics, hosted between 6th and 22nd February, are influencing EMEA trends for early 2026.

Availability in Cortina, and surrounding northern Italian locations like Milan, is incredibly tight; ADR for this period is between €201 and €211, which is up to 49% higher than the same period in 2025. |

|

“Global demand feels healthy and I’m hearing lots of positive noise for big bookings in 2026, which is really encouraging. In Europe specifically, Germany has felt quieter than normal lately but a big new property pipeline for 2026 indicates the strength of the market and a bigger supply should be good news for rates in key cities like Dortmund and Munich. Demand for Lisbon and flanking locations is strong as investment and growth in Portugal continues and Amsterdam continues to thrive, although the National VAT increase from 8% to 21% coming into effect from 1st January is already having an impact on 2026 pricing proposals. It will be interesting to see how a higher tax burden for inbound travel into Amsterdam will influence ADR and demand trends going forward. The beauty of our sector today is the breadth of housing solutions available. We’re continuing to find innovative ways to support consumer need beyond the traditional serviced apartment model, so there are |

|

accommodation solutions for all echelons of guest budget and length of stay. I expect a further diversifying of product and service offerings in 2026, in turn broadening guest demographic and ultimately bolstering the ways we can support diverse consumer requirements.”

|

|

Wider trends influencing EMEA markets

- Dubai enters into the next phase of it's DIFC expansion which will boost new Gulf supply, investment opportunities and related project worker demand

- Saudi Vision 2030 mega-projects continue to transform the KSA

- The Autumn Budget is revealed in the UK which could drive rates up if some operators have more cost pressures to offset

The DIFC expansion promises continued acceleration for corporate demand into Dubai

Dubai’s economic significance continues to advance as it rises to 11th in the Global Financial Centre Index and fourth for global FinTech. The Dubai International Financial Centre (DIFC 2.0) expansion aims to further strengthen its position by developing more office, residential, and hospitality space, better parking and transport hubs. Positive for new Gulf supply and investment opportunities, and will boost accommodation demand from construction, professional services and fintech assignees.

Saudi Vision 2030 mega-projects continue to transform the KSA region

More movement in the Middle East market comes in the form of Saudi Arabia’s real estate and infrastructure Vision 2030 mega-projects which are dominating the regional outlook. Not only are they driving demand now largely from construction, professional services, and fintech sectors, but they represent significant sustained opportunity as the development takes more shape.

In a recent report, Knight Frank forecast that Riyadh’s population will grow from seven million in 2022 to more than ten million by 2030 – six million of those expected to be expats, so the KSA region’s importance in corporate travel and mobility demand will continue to grow over the coming years.

How the hotly anticipated Autumn Budget could impact the UK serviced apartment sector

In the UK, Chancellor, Rachel Reeves, announced her anticipated Autumn Budget on 26th November. Some of the key takeaways and possible impacts on the serviced apartment sector include:

|

100% first-year tax allowance continued for upgrades to kitchen, laundry, and energy-efficient appliances, which could be a welcome relief if you’re an operator with plans to refresh your units. |

|

A further increase to the National Living Wage will increase the running costs of serviced apartment buildings in terms of salary spend for property staff, which could drive rates up as operators look to offset these costs. It could also accelerate the shift to more tech-enabled stays and the automation of certain jobs. |

|

The restructure to business rates based on the size and value of a property might be a relief for smaller operators but put more pressure on those operating large buildings. Added to that is the power granted to mayors to introduce more tourist taxes for overnight stays in cities like London. So, a few more potential cost pressures for operators to contend with are in the pipeline, as well as a risk of dampened demand as corporates might look to avoid visitor levies in some key business hubs. |

|

The demand for secondary and tertiary markets might accelerate as another result of higher footfall locations being more likely to be hit by visitor taxes. |

Americas Booking Data Trends

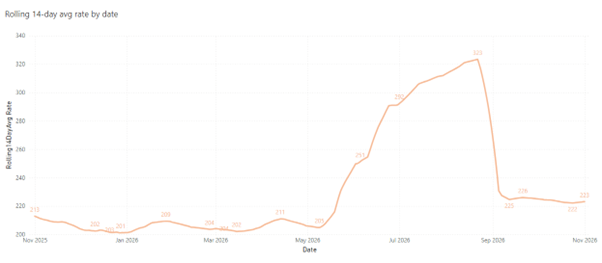

- Demand, pricing and availability across the Americas are being significantly impacted by the 2026 FIFA World Cup – ADR in New York City in June and July, for example, is up to 30% higher YoY.

- The average length of stay (ALOS) for one-bedroom reservations in the Americas last quarter was 64 nights: 14 nights (18%) shorter YoY.

This reduction in ALOS could be a result of lower relocation demand, as relocation spend into the Americas reduced 15% last quarter compared to the same period in 2024. - The average lead time for one-bedroom enquiries in the Americas last quarter was 30 days: 27 days (47%) shorter YoY.

This is a significant overall reduction, which could be linked to the reduction of ALOS as shorter bookings typically require less planning and approval; but could also be the result of various uncertainties within the US market like visas and travel restrictions delaying decision-making.

The ADR forecast in key Americas cities

American markets, before annual trends become more dynamic

Our booking data indicates relative stability and modest ADR decreases over the next quarter in key North American markets, but the annual forecast is more dynamic: the seasonal trend of a summer high and autumn plateau is heightened by the 2026 FIFA World Cup.

The FIFA World Cup is already having significant impact on pricing and availability in key cities across the US, Canada and Mexico: match dates are between 11th June and 19th July, which explains a sharper than usual peak in summer pricing.

Many ADR forecasts in FIFA match host cities are showing a spike for 11th June – 19th July 2026 compared to the same period in 2025. Indeed, SilverDoor booking data shows reservations are converting for up to:

- 30% higher YoY in New York City (NYC) – NYC pricing is the most heavily impacted by event surcharges; our US teams have seen nightly hotel rates offered as high as $700 on match days

|

|

Bookers should keep this in mind and try to give longer lead times for requests in and around the summer period; many businesses with annual internships programmes specifically have already confirmed their accommodation for June check-ins as the FIFA tournament coincides with intern season. So, although in the Americas region as a whole we’re seeing an overall shortening of lead time, it’s a different trend for group intern programme requests for which there’s far more planning ahead and buying in advance. Not only is this influenced by the added pressure of the World Cup availability squeeze, but there’s other trends at play in the job market too:

|

“We’re seeing requests for intern programme accommodation far earlier than normal as a consequence of AI’s impact on the entry-level job market. Junior positions are more competitive than ever, and with the added fear of AI reducing entry-level vacancies, students are trying to get ahead to remain competitive. |

|

Our clients are giving far longer lead times for summer programme accommodation because, we’re told by those clients, students are applying to grad or intern roles earlier, so they’re filling their spaces much sooner than ever. This is positive for travel managers: if programmes are being filled earlier, they’ll have better selection, availability and rates for accommodation.”

|

|

Wider trends influencing US markets

- New York’s mayoral election results could mean a city tax system restructure

- H-1B visa price hike could either boost domestic US moves or accelerate offshoring

- Overnight shutdown of Sonder Holdings might mean a slightly tighter US supply for a while

New York’s mayoral election results could cause changes to the State’s tax structure

Following on from the last Update, we now have the result of New York’s mayoral election. Democrat, Zohran Mamdani, has been elected after his campaign promised locals a restructure of the tax system to ease cost of living issues. Potential impacts on temporary housing supply and corporate demand levels in NYC if any tax changes come into effect after Mamdani takes office on 1st January include:

- Rent freezes to preserve the affordability of housing for locals formed part of Mamdani’s campaign, which some are concerned could lower the real estate investment appetite and therefore decrease the number of new corporate housing developments.

- Demand could be dampened if unfavourable tax changes encourage businesses to diversify operations or relocate offices out of the city, and approvals of mobility or travel plans could be delayed if businesses are cautious about this sort of investment – although early reports say this is unlikely and that many businesses are still committing to long-term plans in New York.

H-1B visas have increased to a price many businesses will not be willing to front

The increase to H-1B visa fees is likely to have significant impact on inbound moves to the US; tech and medical workers from nations like India are due to be most affected. H-1B visas will now cost $100,000, a price many businesses will not be able or willing to front. The implications could be more domestic US moves or the offshoring/migration of operations out of the US, and could go some way to explain the 15% YoY decrease we saw in US relocation spend last quarter as businesses reconsider their talent mobility plans.

What felt like an overnight shutdown of Sonder Holdings might shake the US supply chain

The seemingly sudden liquidation of operator Sonder Holdings announced in November involved an almost overnight shutdown of US operations after Marriott ended their licencing agreement. Sonder properties in the US were closed almost immediately and in-house reservations ended without warning; it remains to be seen what will happen to Sonder’s full portfolio, but corporates should be aware of slightly tighter supply in Sonder’s US markets (LA, NYC, Chicago, Washington, San Francisco, Boston, Miami, Philadelphia and Palm Springs).

The shutdown could be seen as indicative of a challenging market for operators, but the dissolution was not only the result of a long series of financial challenges, it also came at seasonally tougher times for occupancy and coincided with the US government shutdown which was already creating a tricky travel market.

APAC Booking Data Trends

- Tight near-term inventory in many core APAC markets due to the festive period and Australia’s high season.

- The average length of stay (ALOS) for one-bedroom reservations in APAC last quarter (1st August – 31st October) was 53 nights: 6 nights (10%) shorter YoY.

Similar to the Americas region, relocation spend in APAC was 7% lower this year compared to 2024 perhaps due to a localisation of talent or tighter mobility budgets. - The average lead time for one-bedroom enquiries in APAC last quarter was 42 days: 5 days (14%) longer YoY.

Longer lead times and more forward planning in APAC is linked to the typically tighter supply in the region and the need to factor in visa applications for relocations, which encourages bookers to secure their accommodation earlier.

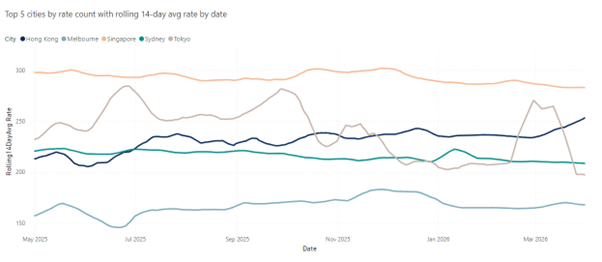

The ADR forecast in key APAC cities

cities over the next quarter

Our data is currently showing a modest negative ADR trend in Singapore as we move into 2026 and towards next spring. Traditional seasonal trends show us that a dip in pricing during spring and summer is unlikely, so what might be influencing this forecasted decrease?

|

“We’ve seen quoted rates in Singapore for springtime 2026 that are far above where the market seems to be headed, so it may be that we’ve not yet converted as many bookings as usual for requests during this period. May-September is also peak season for relocations in APAC, but many of these moves may not have been signed off yet so the influence on ADR is likely to come into effect nearer the time. |

|

Some operators might be trying to increase their yield YoY, but will likely relent nearer the time if they still have occupancy to fill; so, if you’re a corporate struggling to secure rates within budget for the next quarter, we’d advise holding a unit with a seven to 14-day cancellation policy then requesting again elsewhere closer to check-in when operators will be more open to negotiation.”

|

|

Availability for larger units in Singapore is very tight: three-bedroom apartments in particular are almost completely sold out over the next one-two months, as expats are being joined by their families over the festive period and New Year.

Elsewhere in APAC, availability is scarce in Tokyo making the pricing outlook more dynamic as Japan’s labour shortage drives more inbound moves into Japan. Inventory is limited in Sydney and Melbourne as Australia is in high season, and also in Hong Kong which is starting to pick up after a period of stagnant demand earlier in the year. Hong Kong enquiries for the second half of 2025 were 24% higher than the first half, an increased demand that we expect to continue into 2026.

Wider trends influencing APAC markets

- Semiconductor stocks hit record highs and Taiwan demand continues to rise

- A shift away from isolated APAC market negotiations could mean more requests for multi-country rate offerings

- Diversification of demand across India highlights the need for more supply chain standardisation

Semiconductor stocks hit record highs

Semiconductors remain a top news item as the stock prices of chip manufacturers like Nvidia continue to soar. Nvidia, an American technology company which outsources much of its semiconductor production to Taiwan Semiconductor Manufacturing Company (TSMC), recently made headlines with a record $5tn market value. Some question the longevity of the AI and subsequent semiconductor boom, but for now it’s dominating stock markets and will be a key demand driver in Taiwan as we head into 2026.

According to our booking data, we saw a 12% YoY increase for Taiwan enquiries last quarter, an upward demand trend we predict will continue to accelerate over the next year. We’re only now starting to see international accommodation brands enter the Taiwanese market, but serviced apartment inventory is still limited here. Frasers Hospitality is due to open in Taipei with a 200-unit property in 2027 and there may be others in the pipeline too, but corporates should expect a continued squeeze on availability until supply grows.

A shift away from isolated APAC market negotiations towards multi-country accommodation strategies

As corporate demand across APAC continues to accelerate, regional accounts are increasingly looking for multi-country accommodation strategies with bundled rate offerings. Whereas isolated pricing negotiations per market have previously been the only viable strategy, there’s more opportunity now for corporates to capitalise on the developing serviced apartment presence across the region.

We might start to see more consolidated, regional APAC programmes akin to those more commonly found in the EMEA market as businesses seek more consistency and predictability for traveller experience and greater cost saving opportunities. This approach will only be viable if the serviced apartment supply chain broadens and standardises to fulfil the demand.

Demand across India is starting to diversify out of key business hubs – but what does that mean for compliance obligations?

We’re seeing strong accommodation demand in India from the tech, consulting and BFSI sectors, which are driving short-term relocations and project-based travel into Bangalore, Hyderabad, Pune and Gurgaon. High pricing in these central business zones is moving more demand out to secondary pockets like Whitefield (outskirts of Bangalore) and Gachibowli (outskirts of Hyderabad), as well as tertiary markets like Kochi, Coimbatore and Ahmedabad where inventory is currently limited, so supply chain growth opportunities are strong across India.

|

“The APAC serviced accommodation market is certainly maturing, but it is challenging to ensure consistent standards as there’s still a significant variation of compliance across the supply chain. |

|

Duty of care expectations are rising in India, with businesses asking for verified suppliers and standardised quality assurance. Until more standardisation is possible, clear communication between suppliers, agents and guests is critical to avoid misaligned expectations, particularly amongst international assignees.”

|

|

Data source: SilverDoor booking data

On average, SilverDoor receives and records 32,000 enquiries totalling two million enquired room nights every year. Our global market rate analysis tool captures every rate we’re quoted for those nights (regardless of whether a reservation is made) and creates an average daily rate (ADR) for every given calendar date.

The tool is currently analysing 10,411,606 individual ADRs, offered for enquiries or reservations with check-in dates of February 2025 up until December 2026, giving us an indicative picture of historic, current and future global serviced apartment pricing trends.

To draw fair comparisons, all analysis in this report uses SilverDoor booking data in relation to the one-bedroom apartment category only. One-bedroom apartments are the most popular category and represent the largest proportion (more than 70%) of our enquiries and reservations, giving us the greatest pool of data to build an accurate picture of trends.

_______________________________

SilverDoor's Market Update is a comprehensive review of the global travel landscape using our own booking data, wider economic context, and our experts' experience and predictions to build a picture of serviced apartment trends worldwide. Reflecting on the past quarter and forecasting for the year ahead, the report advises corporates on rates, supply, demand and traveller preference to inform booking practices.

SilverDoor captures more than 127,000 datapoints from an average of 593,000 enquired room nights each quarter, the largest and most extensive sets of data available in the sector. This means we can provide the most accurate trend commentary and forecasting for those in the know across the business travel and mobility industry.

Connect with us on LinkedIn to keep up with SilverDoor news, learn more industry insights and discuss market trends. If you would like specific topics or trends to be discussed in a future SilverDoor Market Update, get in touch with us at [email protected].