In this report, we share the current pricing landscape for the start of 2026 and focus on some of the wider trends influencing global serviced apartment demand and rates right now:

- Events-related price surges and availability squeezes: the 2026 FIFA World Cup to the 2028 Summer Olympics

- The war for talent in the technology industry

- AI and the data centre boom

- India’s biggest growth industries from the 2026 Union Budget

- The UK-China Free Trade Agreement

- European 2026 regulatory updates: Amsterdam overnight accommodation VAT increase and stricter German rental restrictions

The SilverDoor Market Update has all the trend- and data-driven insight for corporate accommodation buyers, travel managers and serviced apartment operators to stay agile in changing global markets.

SilverDoor Snapshot

The data centre race is on, the war for highly specialised tech talent has never been more competitive, budding UK-China trade relations and fresh economic growth plans in India offer a welcome dose of opportunity, while the accommodation market in the Americas is feeling a World Cup squeeze.

Businesses are certainly on the move and global demand trends are pointing to a strong 2026 for corporate travel and accommodation, this Market Update report explains why.

Global Pricing Pulse Check

|

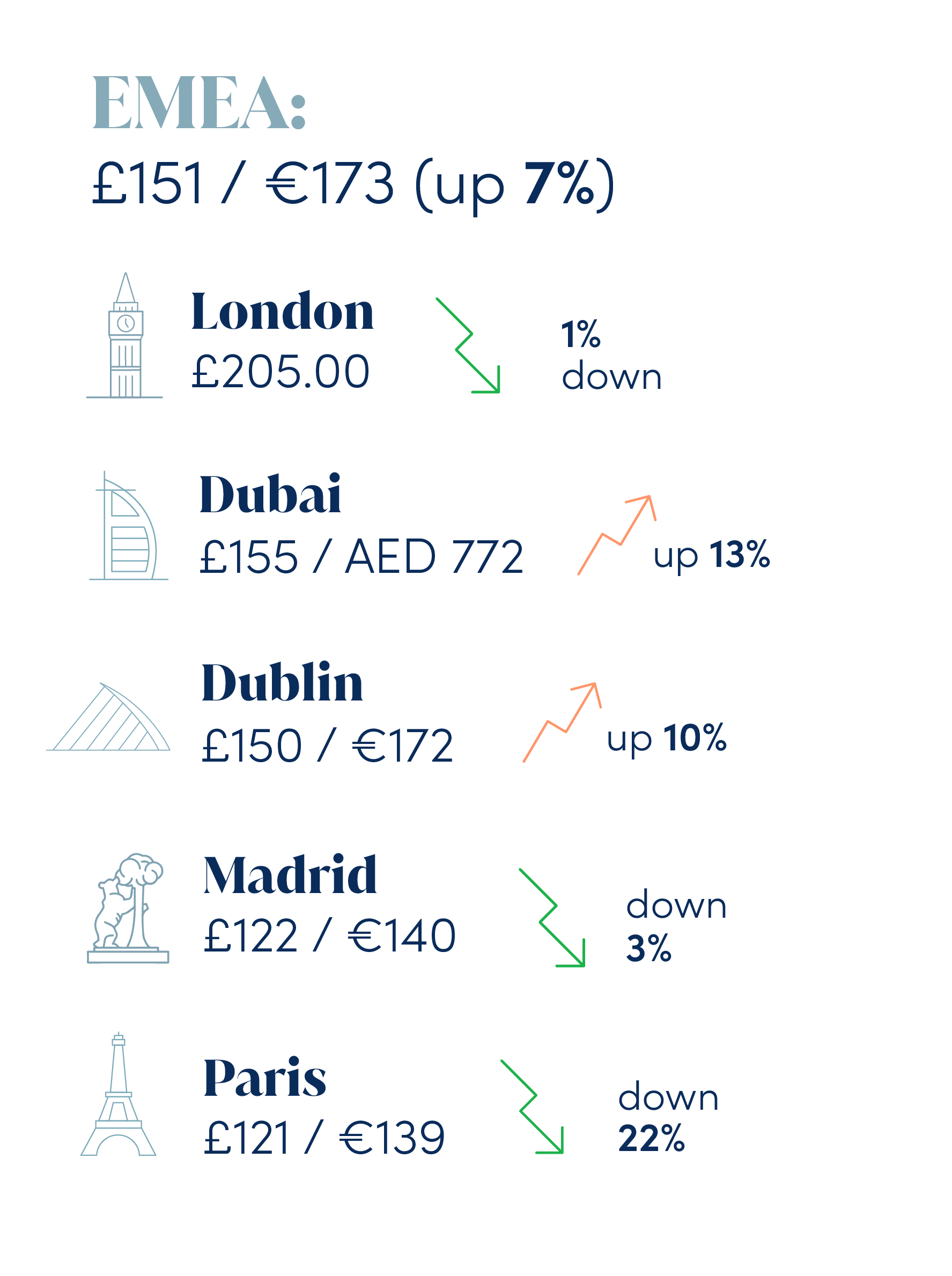

Our booking data shows general YoY ADR increases in the EMEA region: |

|

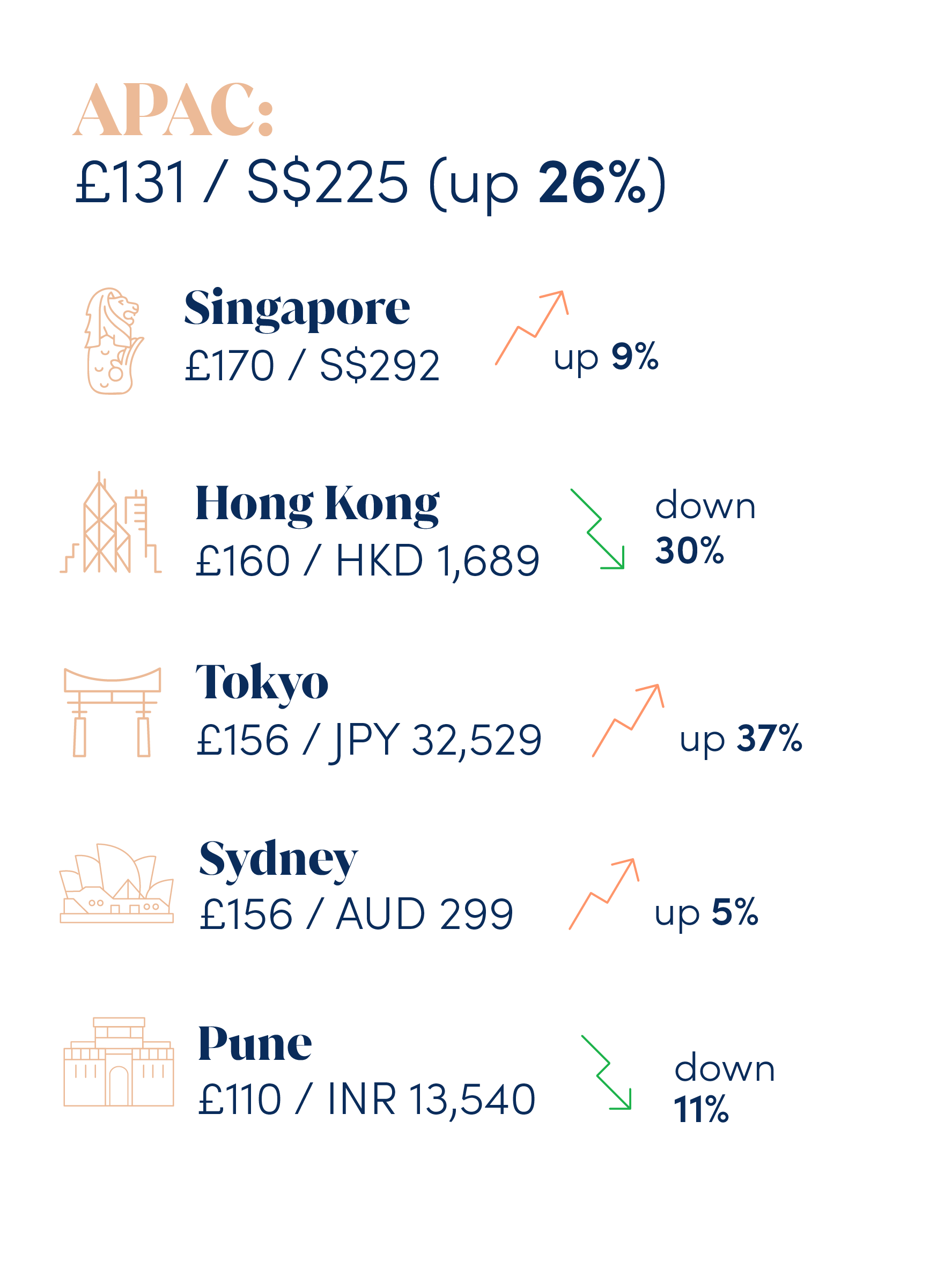

Significant YoY increase in ADR for APAC as a whole, as Lunar New Year demand will have driven rates up in many Asian markets:

|

|

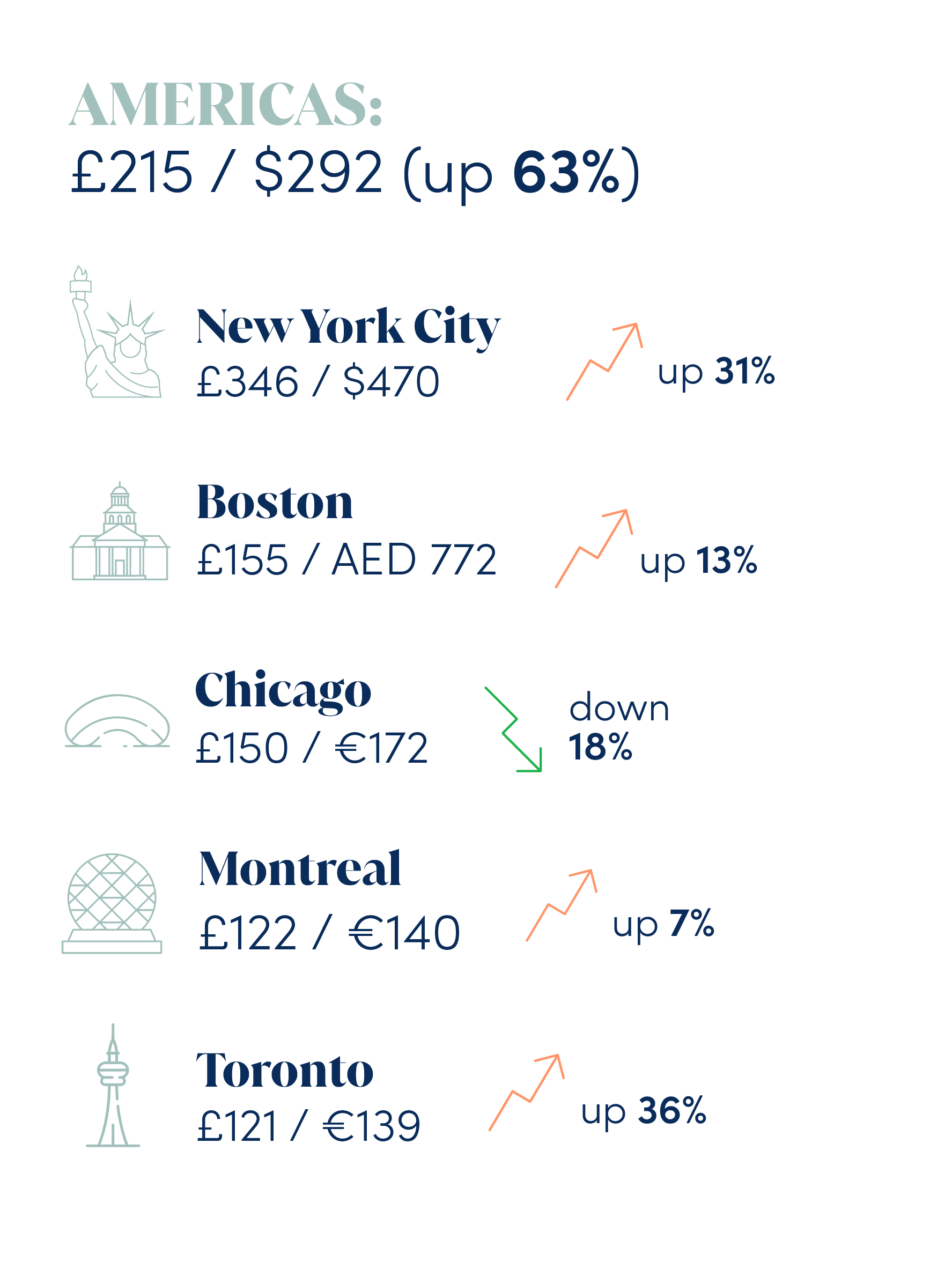

Another big regional YoY ADR increase in the Americas:

|

Getting Ahead of Global Event Impact: What Can we Learn from the Milano Cortina 2026 Winter Olympics & FIFA World Cup?

Major global sporting fixtures, conferences, music/arts events, and cultural holidays have significant impact on pricing and availability in key business destinations and can throw travel plans completely out of whack.

We saw pricing surges around February’s Milano Cortina Winter Olympics and accessing FIFA World Cup match locations across the US, Canada and Mexico is already very challenging in terms of pricing and availability for June and July, so it’s clear that major global events aren’t something you can ignore as a travel manager or corporate accommodation booker.

As well as World Cup related availability squeezes and pricing surges, there are also still concerns about visa applications and approval delays for the millions of international tourists planning their trip to the Americas and Canada. The schedule was only released in December for matches starting in June, but some visa applications are currently expected to take over 200 days to be processed so it’s a very real risk that immigration services won’t be able to fulfil the World Cup visa demand.

If you needed more of a reason to get your strategy in place now for tackling travel plans around major global events, the impact of the 2028 Summer Olympics on LA’s short-term rental market is already becoming clear. Deloitte have published a report predicting a total of 2.1 million people looking for paid accommodation during the LA28 Olympics. This equates to an average of 388,000 people needing housing every single night for the 19-day period, but demand for 13 of those days will exceed 400,000 people and for five of the days will exceed 500,000 people.

The current supply of hotels and short-term rentals is estimated to account for 396,000 people per night, so corporates should start to get ahead of the Games now. Here are some event-related strategies you can build into your mobility and travel planning:

Using historic data is a game changer for avoiding the same challenges year after year. It takes a bit of time investment to do this for the first time, but working with suppliers and going back through your travel management or expense data from the past three to five years will help you to identify past patterns and minimise future risk.

It’s helpful to analyse all elements of the impacted trip like ground transport, air travel, and subsistence, but, for accommodation specifically, your accommodation partner can provide data on things like:

- Average nightly rates paid on and around global events, so you have historic benchmarks for future requests (also make sure to check how many events-based surcharges were added and in which city/by which operator)

- Number of employees across the organisation booking trips that fall during peak event periods

- Location of bookings – how far were they from corporate activities?

- Reason for travel – if trips weren’t related to the event, were alternative dates or locations considered?

- Spikes in over-budget or out-of-policy accommodation requests – were there attempts to avoid?

- Rejected bookings resulting in corporate activities cancelled or moved to remote – what was the impact (wasted cost of a ticket or flight, dent to client relationship or brand image, etc)?

- Last-minute lead times – were they tight turnarounds for a reason, or could this have been avoided?

Rather than tackling each event in isolation, work with suppliers and clients to build the global events calendar into your overall travel strategy. Once you’re armed with both the real-world experience of booking around major events and the tangible data to back it up, you can put a strategic framework in place to protect yourself from future market volatility.

Event dates are usually set well over a year in advance, so map the global major events calendar against your own travel plans around 18 months ahead – including buffer dates before and after the event period itself to account for set up/warm up and derig/warm down demand, and a radius around the actual event location for overflow demand.

- Some degree of peak pricing is usually unavoidable, so allocate higher, more realistic budgets for high-risk locations/periods by building major events into your annual travel budgets. Use data to justify higher budget requests and share data-driven advice with your own end-clients in annual reviews or pricing negotiations to manage their spend expectations.

- Be smart with budgeting – if you plan to minimise accommodation spend by staying 20+ miles outside of impacted locations, you might need to factor in car rental or increased transport expenses.

- You can also be proactive to speed up the booking process by flagging high-risk locations/time periods and securing pre-approval for unavoidable over-budget requests related to event surges. Indecision during peak periods is a killer, so being prepared will give you the advantage: pre-approvals mean you can move quickly and avoid wasting time getting approval at the time of booking when availability is being snatched up quickly.

- Get your requests in with local providers early and put housing on provisional holds 18 months out from an event, before confirming guests and numbers around 12 months ahead. Make sure event planning is a joint effort across departments, so you have business-wide numbers and can negotiate by leveraging bigger booking volumes.

- Don’t just prepare for major fixtures, local holidays can cause similar headaches when entire towns are booked out in an already limited supply chain. Our reservations team always point out things like the Farnborough Airshow in Hampshire, England (20th-24th July), which impacts availability in the London commuter town and nearby secondary cities like Reading, Woking and Guildford when peak summer demand already makes booking during this period a challenge.

Extend trips to avoid checking in during peak times – you’ll likely end up spending less overall on accommodation and airfare for a longer stay, benefit from a more productive trip with higher ROI, and boost assignee morale with a more relaxed trip.

- Operators may enforce longer minimum stay restrictions during peak periods and around major events anyway which you might need to factor in, so plan corporate trips to make the most of longer stays (book more client meetings, schedule team building with international colleagues, arrange co-working spaces, etc) rather than wasting unproductive days.

Be transparent with your business partners, clients or suppliers – if you’re keen to avoid peak event-based pricing and overly busy business hubs, chances are they are too. Assess the reason for your trip and how critical or time sensitive it is, then work with your associates to shift things around where possible.

- If your trip isn’t event-related but happens to fall during peak event demand and can’t be rescheduled, consider alternative locations in neighbouring towns/cities with transport links to the places you need to be during your trip. Not only will you save on accommodation costs by avoiding premium prices, but you’ll probably enjoy less congested roads, a more relaxed environment for meetings, a quieter area for downtime, and easier restaurant bookings.

Annual major events to make note of now and start factoring into your future plans:

- Coachella – California, 10th – 12th & 17th – 19th April 2026

- Men’s UEFA Champions League final – Budapest, 30th May 2026

- FIFA World Cup – USA, Canada & Mexico, 11th June – 19th July 2026

- Edinburgh Fringe Festival – August 2026

- Tour de France – departing in Barcelona on 4th July, then finishing in Paris on 26th July 2026

- Commonwealth Games – Glasgow, 23rd July – 2nd August 2026

- Solheim Cup – Cromvoirt (the Netherlands), 11th – 13th September 2026

- Oktoberfest – Munich, 19th September – 4th October 2026

- World Marathon Majors: Tokyo (1st March 2026), Boston (20th April 2026), London (26th April 2026), Sydney (30th August 2026), Berlin (27th September 2026), Chicago (11th October 2026), NYC (1st November 2026)

- Tennis Grand Slams: Australian Open in Melbourne (January), French Open (18th May-7th June 2026) Wimbledon in London (29th June-12th July 2026), US Open (30th August-13th September 2026)

- The main Fashion Week seasons are February/March and September/October – New York (early February & early September), London (mid-February & mid-September), Milan (late February & late September) and Paris (early March & late September-early October)

- Summer Olympics 2028 – Los Angeles, 14th – 30th July 2028

See a full list of major 2026 events happening around the world expected to influence global travel, rates, and availability in SilverDoor’s latest Impact Calendar.

The War for Tech Talent: the Current Technology Landscape is Stimulating a Rise in VIP Requests

At the end of January, tech giant Amazon announced its second major wave of redundancies since October last year. Tightening their workforce is part of a productivity-boosting, post-pandemic corrective strategy – an operational shift representative of wider tech-sector trends.

The layoffs aim to flatten the organisational structure – reducing the mid-level workforce and, as Amazon put it, removing unnecessary layers of bureaucracy so they can move faster for customers. This aligns with a continued slowdown in corporate jobs – dubbed the “white-collar recession” – and also speaks to businesses correcting their pandemic over-hiring and using AI-driven productivity to trim their workforce.

The job market is highly competitive for senior specialist roles in fields like AI, machine learning, data science and cyber security, as well as data governance and technology ethics.

What does this mean for global mobility and corporate housing?

- More movement between companies in leadership and C-suite jobs as specialised roles are in such high demand means more temporary housing demand for tech-related relocations around the world, but particularly in dominant tech hubs like San Francisco Bay, Silicon Valley, NYC and Seattle, Beijing and Shanghai, London and Dublin.

- A focus on fewer highly specialist roles in place of a larger mid-level workforce means more internal mobility – there’s more need for senior staff to oversee projects and lead expansions into new markets, meaning more project-based business travel and long-term reassignments in secondary tech hubs like Paris, Berlin, Munich, Zurich, Bengaluru, Tokyo, Singapore, Toronto, Montreal and Vancouver.

- A smaller but higher value senior workforce means more tech-related VIP demand, and we’ve already noticed a significant increase in these requests (specialist executive management of long-term apartment stays, luxury accommodation, and additional services) – with one tech client’s 2025 VIP bookings tripling compared to 2024.

Data Centre Demand: AI’s Impact is Spilling Out into Construction, Energy & Professional Services Fields

Sticking with tech and AI trends, the data centre construction market is exploding right now and is forecast to be a $456 billion market by 2030 with current 11.8% compound annual growth rates (CAGR). Data centres are what fuel and facilitate modern cloud services and AI technology, but the development, build and running of data centres spills out into fields like:

- Energy

- Mechanical engineering

- Security

- Professional services

- Supply chain and logistics

- Infrastructure

- Health and safety

The average data centre costs $597 million to build and monthly data centre construction spend in the US has been reaching highs of nearly $5 billion, so where are these mammoth digital infrastructures and how many are popping up around the world?

There are currently active 10,506 data centres in 174 countries: the US accounts for 36% of all global data centres, followed by the UK with 5%, but other established data centre locations include Germany, The Netherlands, Japan, Singapore and Australia.

According to JLL global data centre capacity is expected to double between now and 2030, and McKinsey reports the investment needed to regenerate and scale data centres at the current growth rate is as high as $6.7 trillion.

How will this impact global demand trends for corporate travel, assignments, and temporary housing?

- In terms of building new data centres, it’s the construction phase that will see the highest temporary accommodation demand for both transient and mid-term project-workers in the emerging data centre locations like Thailand, Vietnam, Indonesia and India in APAC; Dubai and Riyadh in the Middle East; and secondary markets across the US like Phoenix, Arizona and Richmond, Virginia.

- There’s a lot of discourse around “AI taking people’s jobs” and, whilst this is true in some cases for certain job roles and industries (see the above commentary on Amazon redundancies…), AI is also to thank for employment booms in other areas. The race for data-centre-related talent is huge especially for highly specialised, highly paid project workers, with reports showing construction workers are capitalising off up to 30% pay increases for jumping on a data centre project. These workers represent demand opportunities in the tiers above your standard hotel or apartment, but below tech-related VIP and luxury stays.

- Data centre demand is a tricky one for the serviced apartment supply chain to match, though, as up to 1,000 project workers could be contracted for the 18–30-month construction phase but only around 20-30 operational staff are needed to run the facility once it’s built. This is positive for centres being built near towns and cities where stock already exists, like the five sites planned for Greater Manchester, but sourcing temporary housing solutions near remote sites will continue to prove challenging.

India’s Union Budget: Which Industries Can Expect a Boost in Corporate Housing Demand?

Speaking of data centres, India’s Finance Minister recently announced the 2026-2027 Union Budget which focuses on the data centre boom as a key Indian growth opportunity. Budget headlines include a 20-year tax exemption for foreign tech companies using Indian data centres to serve global customers, and increased investment in skilling and upskilling of workers for AI-specific roles to address the current skills shortage.

As well as AI, cloud computing and data centres, which industries are quids in and how might they influence travel, mobility and corporate accommodation trends in India?

Banking, Financial Services and Insurance (BFSI)

Banking, Financial Services and Insurance (BFSI)

Budget headlines: extension of tax breaks and incentives in GIFT City (Gujarat International Finance Tec-City) and general easing of regulation for international banks and insurance firms.

Demand will come from: project workers/professional services teams involved in construction and set up of new Indian offices or regional headquarters, and the banking/insurance expats reassigned to them.

Demand will be for: executive short-long term stays/relocations in GIFT City and other key financial hubs like Mumbai, Bengaluru and Delhi NCR.

Manufacturing

Manufacturing

Budget headlines: more investment in industrial corridors; Free Trade Agreement (FTA) with the EU widens export opportunities; labour reforms will make local hiring easier

Demand will come from: long-term stays for construction and engineering project workers setting up new factories and facilities; short and mid-term stays for rotating quality control and audit teams

Demand will be for: industrial corridor developments like Delhi-Mumbai, Amritsar-Kolkata, Chennai-Bengaluru, Bengaluru-Mumbai, Vizag-Chennai, as well as other port cities like Goa, Kerela and West Bengal

Infrastructure

Infrastructure

Budget headlines: investment in seven new high-speed rail (HSR) corridors for regional connectivity with tier-II and tier-III cities

Demand will come from: professional services and international contractors involved in the procurement process; specialist engineering and construction workers involved in the build

Demand will be for: tier-II and tier-III locations along the HSR projects where serviced accommodation supply is still very limited – corridors are:

Mumbai–Pune (Tier-II/III cities to benefit: Pune and Nashik)

Pune–Hyderabad (Tier-II/III cities to benefit: Solapur and Aurangabad)

Hyderabad–Bengaluru (Tier-II/III cities to benefit: Kolar and Chikkaballapur)

Hyderabad–Chennai (Tier-II/III cities to benefit: Kakinada and Tirupati)

Chennai–Bengaluru–Mysuru (Tier-II/III cities to benefit: Mysuru and Krishnagiri)

Delhi–Varanasi (Tier-II/III cities to benefit: Agra and Prayagraj)

Varanasi–Siliguri (Tier-II/III cities to benefit: Gorakhpur and Siliguri)

Power and renewable energy

Power and renewable energy

Budget headlines: renewable energy incentives for solar, wind and hydrogen to support India’s commitment to net zero by 2070

Demand will come from: engineers, consultants, installation and operational teams for solar and wind farm developments and green power plants

Demand will be for: coastal locations like Tami Nadu and Gujarat for offshore wind farms, and Rajasthan for solar

Healthcare and pharma

Healthcare and pharma

Budget headlines: tax breaks for research and development (R&D); increase public health spending and access to screenings, long-term care and affordable medicine; boost AI and data use for healthcare

Demand will come from: R&D and clinical trial scientists, and manufacturing/regulatory compliance specialists

Demand will be for: Hyderabad, Bengaluru, Ahmedabad, Mumbai, and Pune

The budget signals confidence in long-term growth for the Indian economy, which is expected to continue as the world’s fastest growing economy this year. We’re already seeing significant YoY increases in demand for many Indian markets and can expect to see further boosts to demand and spend in the region.

We looked at comparative enquiry data for tier-I Indian business hubs from Nov 24-Jan 25 and Nov 25-Jan 26:

- Enquiries for Gurugram are up 216%

- Enquiries for Hyderabad are up 47%

- Enquiries for Pune are up 18%

- Enquiries for Mumbai are up 17%

Enquiries are primarily for one-bedroom apartments (60%), 12% of enquiries include children and 4% include parking requests.

The average length of stay for India reservations is 60 nights – 18 nights longer YoY which aligns with the growing demand for longer term project and relocation accommodation.

UK & China Trade: What New Trade & Investment Opportunities are on the Horizon?

We’ve touched on the India-EU FTA, but India isn’t the only major economy looking to boost trade relationships and access to export markets. The UK prime minister, Kier Starmer, paid a visit to China in January with 50 leaders from major UK companies in tow in an attempt to thaw the previously frosty UK-China economic relationship.

Some of the headline successes from the trip in relation to boosting corporate housing demand include:

- Visa-free travel: British citizens will be able to head to China for business or leisure trips up to 30 days without a visa, making short-term corporate travel easier, cheaper and generally more attractive for UK companies.

- Chinese investments into the UK: companies in energy, automotive, consumer goods and life sciences companies are investing in the UK, which will create engineering, manufacturing and science-based jobs in cities like Liverpool (where Chinese car firm, Chery, is due to open a European headquarters) and boost UK-China cross-border talent mobility between regional facilities.

- Pharma investment into China: AstraZeneca are investing $15 billion into their medical manufacturing and R&D footprint in China, stimulating inbound travel and internal mobility for highly skilled medical workers.

- Renewable energy expansions in China: Octopus Energy (specialising in energy-related tech and software) have joined forces with China’s PCG Power to boost real-time renewable energy trading in a “major step in exporting British energy tech overseas”. Related corporate housing demand, while relatively minimal, would include UK-based software engineers or senior executives visiting Chinese sites in places like Guangdong, but it does represent China’s long-term commitment to clean energy.

Already we’ve seen a bit of a resurgence when it comes to corporate demand for China. Comparing data for Nov 24-Jan 25 to Nov 25-Jan 26, we’ve seen enquiries on the rise across the board:

- For the whole of China, enquiries are up 66% YoY

- In Beijing, enquiries are up 120% YoY

- In Hong Kong, the increase we reported last quarter has continued with a 40% YoY rise in enquiries

- In Shanghai, we saw 29% more enquiries YoY for this period

These enquiries are primarily for one-bedroom apartments, which represent 58% of total enquiries, but 15% of total enquiries included children and 4% of total enquiries included a pet indicating a diverse range of corporate travellers are looking at accommodation in China.

The average length of stay for China reservations is 41 nights.

Bookers should be aware that the serviced accommodation supply chain is still relatively small compared to the hotel industry, so it can currently be more challenging to find lower priced options. Our booking data shows ADR for a one-bedroom apartment in China (Nov 25-Jan 26) was CNY 881.19/$161, but so we expect this to gradually come down as the serviced apartment market grows.

European 2026 Regulatory Updates

Has Amsterdam’s 2026 national VAT increase had an impact on corporate housing trends?

Amsterdam is another European country with strict short-term rental restrictions, and the latest effort to minimise holiday rentals squeezing out local residents is a VAT increase for overnight accommodation which went up from 8% to 21% from 1st January 2026.

We’ve analysed our Amsterdam booking data (Nov 24-Jan 25 compared to Nov 25-Jan 26) to see if the higher tax burden has had an impact on demand and pricing:

- Enquiries for Amsterdam have decreased 7% YoY

- Reservations in Amsterdam have decreased 17% YoY

- One-bedroom ADR in Amsterdam for the past quarter was $217.38 – 11% higher YoY

We will continue to monitor the impact of Amsterdam’s overnight accommodation VAT increase, as well as the city’s current plan to reduce the maximum number of nights that locals can rent out their home on platforms like Airbnb from 30 to 15 nights a year which, if passed, would further limit availability in eight Amsterdam districts. For now, bookers should be aware that the VAT increase applies to 2026 stay dates even if the booking was made in 2025, and corporates should anticipate higher accommodation costs for Amsterdam bookings moving forward.

German municipal rental restrictions

Rental restrictions in Germany are nothing new, however the government is coming down harder on illegal short-term rentals with new regulation coming into effect in May this year.

Amidst an ongoing housing crisis, German municipalities enforce varying levels of short-term rental restrictions – Zweckentfremdungsverbot which translates as “prohibition of misuse” – to try to improve the affordability of permanent housing for local people.

Berlin has the strictest rules, but a 2025 report found that only around 2% of short-term rental apartments have been legally registered and approved so local authorities are becoming stricter. Districts like Neukölln and Friedrichshain-Kreuzberg are clamping down, and some are giving out penalties of up to $500,000 for non-compliant rentals – among the most severe housing violation fines in Europe.

Munich and Frankfurt are other major German cities with strict restrictions, but a new nation-wide rule being enforced from May will make it harder for illegal rentals to operate under the radar without being registered. The law mandates that property information from short-term rental booking sites like Airbnb must be automatically reported to the German authorities, so compliance with restrictions can be officially monitored. What could this mean for corporates?

- If more non-compliant holiday rentals start to be removed from the market and distributed to permanent residents, the short-term rental stock across Germany will reduce meaning fewer options for inbound visitors heading to Germany on business.

- Ultimately this could cause ADR increases as demand might start to outweigh suitable supply.

Something piqued your interest?

These insights are based on extensive data collection and market research, as well as the real-world experiences of SilverDoor people who spot market shifts as they start to form and see the effects of market trends first-hand. You can speak to our team directly to learn more about how these trends might impact your travel plans: contact one our global teams today for informed and impartial advice.

___________________________________________________________

SilverDoor's Market Update is a comprehensive review of the global travel landscape using our own booking data, wider economic context, and our experts' experience and predictions to build a picture of serviced apartment trends worldwide. Reflecting on the past quarter and forecasting for the year ahead, the report advises corporates on rates, supply, demand and traveller preference to inform booking practices.

SilverDoor captures more than 127,000 datapoints from an average of 593,000 enquired room nights each quarter, the largest and most extensive sets of data available in the sector. This means we can provide the most accurate trend commentary and forecasting for those in the know across the business travel and mobility industry.

Connect with us on LinkedIn to keep up with SilverDoor news, learn more industry insights and discuss market trends. If you would like specific topics or trends to be discussed in a future SilverDoor Market Update, get in touch with us at [email protected].