Businesses and corporate accommodation buyers are managing travel and mobility programmes in markedly different conditions to last quarter. Decision makers have been contending with more risk than usual and booking behaviour is being shaped by various economic, geopolitical and regulatory headwinds.

We’ve been watching how current market conditions – both positive and challenging – are influencing why, where, and how much businesses are on the move. What we’re seeing is strong demand for London, China, India and the American West Coast on one hand, but uncertainty around continued oil shortages and immigration delays on the other.

In this report, we provide serviced apartment pricing headlines to support informed budgeting and analyse the key market trends impacting travel and mobility programmes today.

Click to go straight to the trend most important in your world:

- Fallout and reflections of the Middle East conflict

- The changing travel landscape in China

- Strong investment and long-term corporate commitments in London

- How we saw corporate housing demand and pricing play out in the lead up to the FIFA World Cup

- From interns to VIPs: how an unrecognisable labour market is splitting corporate housing demand in two

- Regulatory shifts: UK visitor levy passed, energy efficiency retrofit deadline approaches, and US immigration processing delays

Find data-backed observations on all these trends below with actionable guidance on how to capitalise off their opportunity or mitigate their effects on your programme.

The Why Behind the Price Tag: How Corporates Should Budget Based on Pricing in Key Global Markets

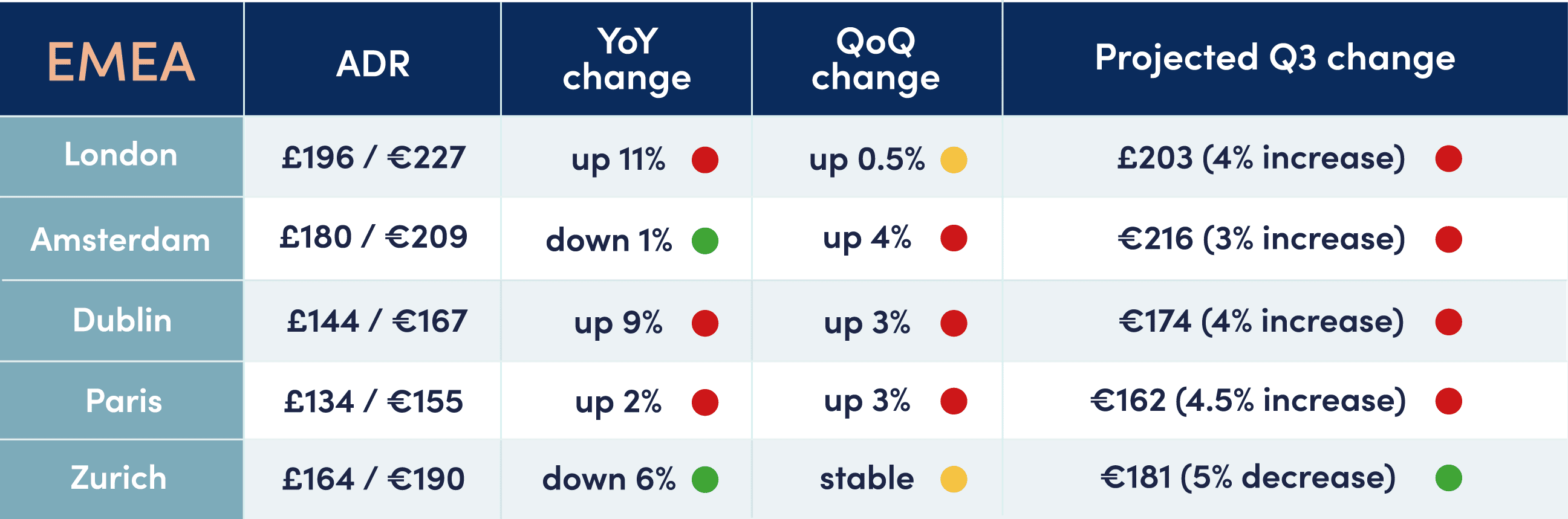

EMEA price headlines

Fairly stable pricing across the board in our key EMEA markets compared to last quarter, with a few larger fluctuations in London, Dublin and Zurich compared to last year. Slight increases projected for the next quarter, which is unsurprising as we’re entering peak season and when you consider the impact of global energy shortages. Buyers should budget higher for the remainder of the summer.

Rates in London have experienced the biggest YoY increase, with growth expected to continue into next quarter. Later in the report we cite why London demand is up and set to keep rising, and we’ve added 2,225 units to our London supply chain since this time last year to support this growing corporate interest. Although, we also note upcoming regulatory changes that could constrict supply in the city, an availability pressure which could continue to push rates up.

After London, at 9% higher YoY, ADR increases in Dublin are the second most significant. In a market already up against tight supply relative to demand, we’ve seen a decrease in Dublin stock since this time last year as operators have released aged product which means more competition for remaining units and ultimately higher pricing.

Despite the increased accommodation costs, both London and Dublin have retained their position in our top five cities by volume demonstrating that demand is strong for both business hubs and buyers are willing to pay the premium.

Zurich tells a mixed story. For a typically expensive market, the 6% YoY rate decrease will be welcome news for buyers with Swiss commitments. Usually, price drops would indicate a quiet market, but our booking data also shows that both enquiries and conversion have almost doubled compared to this time last year.

The uplift in demand may actually be in response to more attractive pricing, and perhaps more programme spend is being consolidated through housing providers rather than direct bookings which unlocks more negotiation power. A further projected ADR decrease means Zurich is looking like a more accessible market for more mobility programmes, so opportunity is strong here.

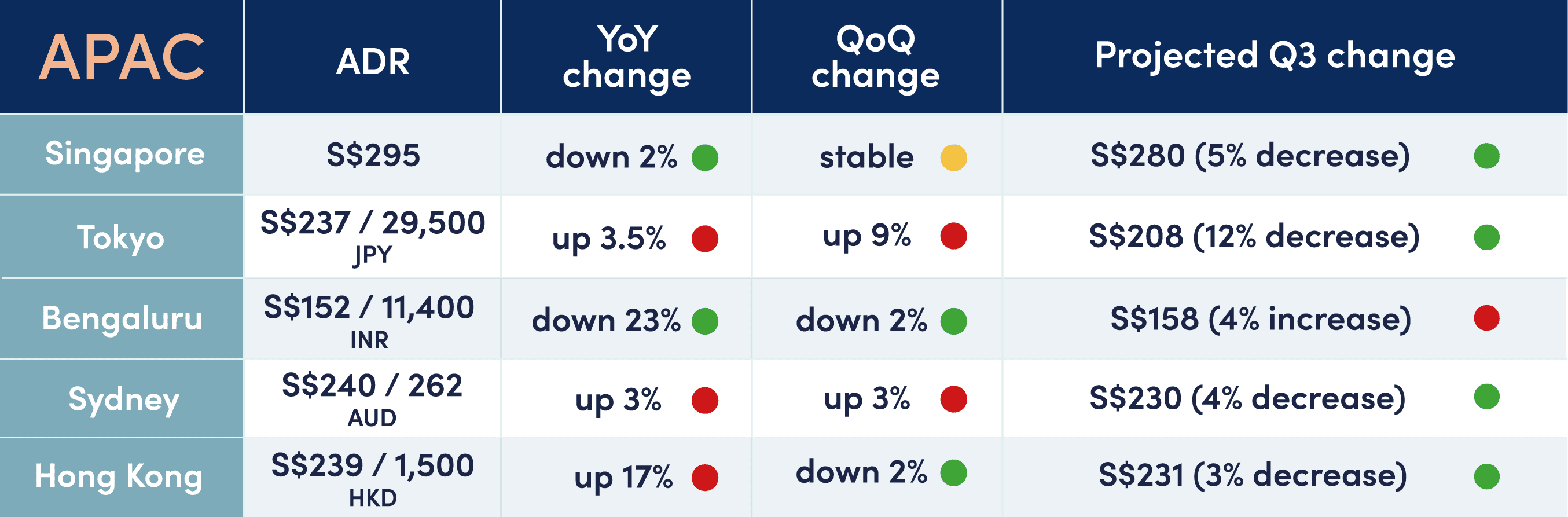

APAC price headlines

A more dynamic pricing landscape in APAC where a number of wider supply and demand factors are at play in our top markets.

Starting in India, it’s great to see QoQ stability at the same time as significant YoY corrective pricing suggesting that the limited serviced accommodation supply chain is starting to grow to match strong corporate demand. We’ve added 681 units to our Bengaluru stock since this time last year, meaning there are more options for buyers to choose from and more negotiation opportunities to be had via managed accommodation programmes here.

We’re still seeing significant increases in both enquiries and reservations across India – up 114% and 457% respectively – primarily from technology companies (clearly the India mobility market is resilient to the potential impact of mass tech sector layoffs), but also from a broader clientele across BFSI and professional services, pharma, life sciences and healthcare.

It’s the opposite story in Hong Kong where we’ve seen a tightening of available supply while demand continues to pick up. We’ve seen a considerable increase in website traffic for accommodation in the region – searches for serviced apartments in China and Hong Kong last quarter were up 83% and 116% YoY respectively, along with increased specific searches for both primary and secondary cities like Shanghai, Beijing, Chengdu, Guangzhou and Wuxi – so it’s clearly a key region of interest. This is now translating into real commitment and intent to book: reservations nearly doubled last quarter YoY despite continued restricted availability.

We’ve seen 160% more bookings in Japan this year than we did in Q2 2025, so the current attractive business climate in the country is clearly stimulating more inbound corporate travel. The 9% QoQ price spike in Tokyo is due to see a seasonal stabilisation over the next quarter, and the additional 1,283 units in our Tokyo serviced apartment supply chain compared to this time last year will further support the strong demand here.

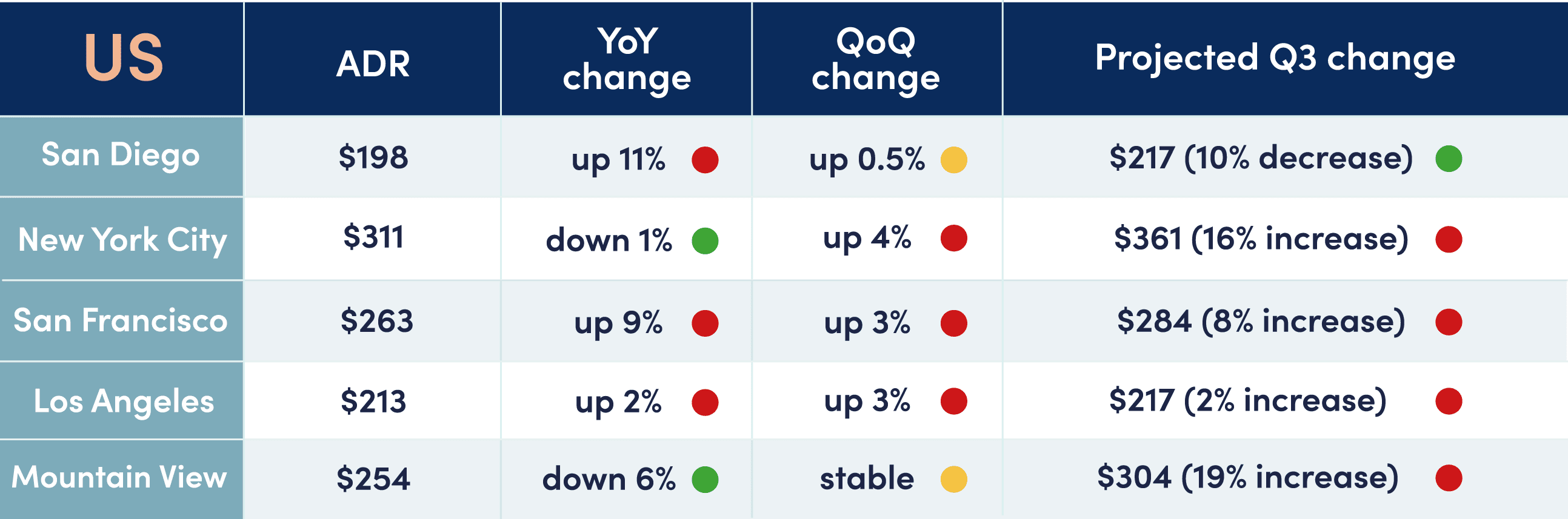

USA price headlines

ADR in our main US markets has held firm compared to the previous quarter, but sustained price increases YoY is indicative of wider inflationary pressures across the States. The heavy California presence in our top markets points to tech-sector-leaning demand in our data suggesting that, despite the major shifts in technology workforces we reported last quarter and have continued to see over the past few months, West Coast tech-related demand hasn't dampened as we might have anticipated.

The projected rate increases we’re seeing across those key US markets are likely a hangover from World Cup price and demand spikes, and align with the energy shortage which will be adding pressure to building running costs that operators will have to offset. Buyers with big US volumes should expect continued volatility.

As well as these top markets, we’re also seeing greater interest for Chicago, Dallas, and Mexico City, as well as strong demand across Canada, compared to this time last year – perhaps related to the imminent World Cup but also extending beyond match dates.

Market Conditions Impacting Travel & Mobility Programmes Right Now

The Middle East: Conflict Fallout and Reflections

Tensions in the Middle East escalated towards the end of February and the fallout has rippled out in many different directions.

Near-term fallout: crisis management protocol, contingency planning and business continuity

Whilst Middle East enquiries were expectedly down for the past quarter, with a 14% YoY decrease they weren’t down as significantly as we would have expected. Reservations for locations like the UAE were also marginally up, demonstrating that there are assignees still heading to the area despite the uncertainty.

We didn’t see huge volumes of evacuations or displacement; instead, we’re continuing to see mostly intel gathering and contingency planning:

- For our clients in industries like banking, trading, and financial services, the crisis management procedure extends beyond employee safety and into legal and regulatory logistics. Many did close branches, evacuate offices and ask staff to work from home/remotely, but financial licenses are very strict in places like the UAE and Saudi Arabia meaning firms weren’t only gathering intel about where they could move people to safety, but where they could safely move people to locations that still allowed them to legally do their job.

Often, licenses are for particular jurisdictions and might only cover people to work from a registered office rather than an apartment or co-working space. This can have significant financial implications as these organisations can’t afford to have a large portion of their workforce out of business for hours, let alone days or weeks. Many firms might have backup contingency offices set up in the same license zone for business continuity during a crisis, but they still have the risk to manage of retaining staff in active conflict locations. - We’ve seen some scouting out for relocation accommodation in Egypt but, instead of cross-border evacuations, some clients are still now looking at moving people from central Dubai to smaller towns like Al Ain (east of Abu Dhabi on the UAE border with Oman), Ras Al-Khaimah (north of Dubai on the coastal tip of UAE) and Fujairah (east of Dubai, on the UAE-Oman boarder south of Ras Al-Khaimah).

These are only exploratory as many businesses continue mostly as normal while closely monitoring the situation; as our reservations show, we’re seeing that businesses are still sending assignees to the area, especially for critical or time sensitive projects in industrial sectors like construction, manufacturing, and energy.

Longer-term fallout: buyers look to control the controllable as global oil shortages create uncertainty for transport costs

In what the International Energy Agency has called “an unprecedented supply shock”, the world is facing global oil shortages as the Iran conflict is limiting production in the Middle East and the Strait of Hormuz remains restricted.

Irish airline, Ryanair, has attempted to calm consumer concerns by explaining that European oil supply is less dependent on the Middle East than people might think, but the risk for many airlines is significant if oil prices remain high and markets remain volatile. The news of Spirit Airlines in the US ceasing operations is an example of how some carriers simply aren’t in a position to survive unexpected market shocks like this one.

What this means for the corporate travel industry

- Travel teams with requirements in affected Middle East locations should prepare for potential disruption amidst ongoing conflict in the region. We recommend regular supply and pricing check-ins with your temporary housing supplier, so you’re aware of market conditions should anything escalate and urgent displacements are required.

- Similar to the financial licensing issue we covered above, something for HR and mobility teams to consider is amending the visa of displaced assignees that are forced to work remotely while on a visitor visa (or local equivalent). There can be immigration and tax risks involved especially with extended stays on the wrong visa, so make sure to track displacement timelines and seek advice early.

- What our Client Services team is reporting on a more global level is a stronger emphasis on temporary housing cost containment. Airfare and ground transport costs are generally higher and unstable, so buyers are trying to save where they can on other elements of the travel and mobility journey which is impacting accommodation budgets.

Something that the Middle East crisis makes very clear is the importance of a robust supplier network and a proven crisis management framework. Your organisation’s resilience against crises is only as strong as your supply chain’s, so the safety of your assignees depends on building a supplier infrastructure prepared to manage, respond to, and support you during a crisis.

China: is the Tide Turning for Inbound Travel?

China may have emerged surprisingly victorious amidst global oil shortages as a result of the Middle East conflict. According to the Financial Times, as the price and supply of fossil fuel has increased, so too has demand for China’s sustainable technology like solar panels, battery electric vehicles and lithium-ion batteries.

In a similarly positive outlook, China corporate travel has mostly been outbound since the pandemic, but recent visa developments seem to be stimulating more inbound travel.

- China enquiries were up 36% YoY for the past quarter, and total reservations have doubled YoY

- Conversion rates are also much stronger in 2026 than we were seeing in 2025, demonstrating corporates have moved from what we were told were more exploratory enquiries to now real demand

The easing of entry requirements will be driving a lot of this demand. First, since February, nationals from the UK and Canada can travel visa-free for business or pleasure to China for up to 30 days. Second, in early March, China’s updated Foreigners Entry-Exit Administration Regulations were released with the new K visa for global science and engineering graduates.

The K visa grants multiple 180-day stays for a period of five years; the online application process is designed to be quicker and visits for R&D, teaching, entrepreneurship and academic exchange are automatically authorised. Attracting young talent in these fields aligns with China’s strong commitment to green energy investment and might mean we start to see more intern and grad groups into China moving forward.

We’ve already serviced a large group enquiry into Shanghai for mature students on an entrepreneurial course, including apartments near university locations for both students and high-profile faculty members and business partners.

Culturally, it’s very important to have face-to-face representation for meetings in China and regular in-person contact to build relationships, so further easing of entry requirements is great news for organisations looking to expand operations or boost business ventures in China.

London: A Renewed Corporate Commitment to the British Capital

Research into new job postings shows that mentions of remote working in job postings have fallen by more than 60% in 2025 since their 2022 peak, demonstrating the shift back to office-first working. Other reports support this trend by showing healthy year-on-year growth in deals for office spaces in London, with 43% of central office developments due to be delivered in 2026 already pre-let.

Towards the end of 2025, deals were signed for large office space in London’s Oxford Street and Liverpool Street by investment company Ares Management and law firm Gibson Dunn respectively; the likes of Visa, JPMorgan Chase, and Qatar’s sovereign wealth fund also announced plans to build or update buildings further east in the Canary Wharf financial district.

SilverDoor Client Partnership Managers have heard first-hand from several clients across fintech, energy, and law that they have plans to open or relocate to new offices in London within the next two years.

We’re likely to see sustained near-term interest and a long-term boost in travel and mobility to the British capital

London demand for the past quarter has been healthy, with a slight dip in total enquiries but a 26% YoY increase in reservations indicating strong corporate commitment and intent to book. Perhaps a sign that businesses are enjoying more budget confidence this year and can afford to be more decisive, and evidence that these big corporates are choosing London offices with real intent to have their people working, visiting and staying there.

This demand will sustain as we head into peak summer season, but corporates should take into account forecasted rate increases when budgeting their trips to the city. ADR in London is currently sitting around £196, which is 11% higher YoY and our data indicates the upward trend will continue over the next couple of months.

World Cup Cities Reportedly Fell Short of Hotel Occupancy Forecasts – What About Corporate Housing?

The FIFA World Cup remained a hot topic of conversation for the past quarter. In the weeks leading up to kick off, a market analysis by AHLA cited FIFA room block cancellations, international travel barriers and rising costs as reasons for anticipated demand not translating to strong hotel bookings.

At the time of release for this report, we’re just a day out from the tournament’s first game but how did we see demand and occupancy playing out for the corporate housing market?

- Similar to the hotel space, initial concerns around cities being entirely booked up and surging rates turned out to be much less dramatic.

- We see it with all major sporting events like World Cups and Olympic Games – FIFA’s overestimated held inventory was released about a month out, so supply constraints eased and previously heightened rates were moderated back down in cities like Atlanta, LA, Miami and Toronto. Initial pricing spikes of 50% in Californian markets like Mountain View, Palo Alto, Redwood City, San Bruno and Santa Clara, for example, softened to roughly 15%.

- Boston announced hikes to train fares from $8.75 to $80 for a round-trip from Boston South Station to the Gillette Stadium in Foxborough, which impacted booking patterns. If supporters had tactically booked or planned to stay further from the stadium to avoid expensive accommodation, they were suddenly facing unexpectedly higher commuting costs which pushed more demand around the Gillette. Foxborough also has its own short-term rental restrictions, so demand remained concentrated in downtown Boston, but our operators didn’t report levels exceeding usual peak season.

- Most pricing stabilised below early forecasts in Dallas and Houston, but premium inventory or accommodation within walking distance to the stadiums remained high with some listings reaching $1000 per night on match dates.

Whilst World Cup demand is less concentrated than for a single Olympic Games host city, the 2026 FIFA tournament can be used as a blueprint for corporate buyers to approach the LA28 Olympics: corporate housing operators are open to negotiation for longer stays, holding off to book until mass held stock releases can yield huge savings, and many operators will actively protect corporate clients from rate surges because they are long-term, repeat bookers rather than one-time, leisure bookers.

From Interns to VIPs: An Unrecognisable Labour Market Influencing Increased Demand from Both Ends of the Seniority Scale

In February’s Market Update, we explored the changing state of tech sector workforces and cited Amazon’s mass 2025 redundancies as a sign of the times: as AI is increasingly able to take on bigger workloads, major tech players are opting for fewer, more senior and specialised human employees.

At time of writing, there have been more than 138,000 tech sector layoffs in 2026 alone. Huge brands like Linkedin, Snap Inc, Cloudflare, and PayPal are changing their entire operating model, and the workforce they want to run it, in favour of AI-optimised productivity.

This is happening at the same time as reports show the applicant pool for entry-level jobs in the US has nearly tripled since 2022 – demonstrating how competitive the market is for graduates and junior positions.

This matches up with reports that UK university levels are falling as young people could be responding to labour market bottlenecks by opting out of a degree because it’s no longer a strong enough differentiator to warrant the debt. Immigration uncertainties are also impacting international college admissions in the US, so there are several factors at play leading to a reduction in higher education students.

Consequences for talent mobility and corporate housing

So – companies are focusing their headcount investment on more senior-level employees and fewer mid-level and entry roles, while young people are increasingly choosing the school of life and going straight into work after school rather than higher education. Interestingly for us, we’ve seen this manifest in a rise in requests for both ends of the traveller profile seniority scale:

- As senior, highly specialised workers remain a hot commodity for new roles, large-scale tech projects, and strategic expansions, our 2026 VIP enquiries are already 33% higher than total 2025 levels. These VIPs include guests in data governance, legal associates, or high-profile business partners and need almost an entirely different service delivery than other bookings.

We predict this uptick in executive travel demand to continue, which makes it a great time to ensure your housing partner is equipped to service these requests. - Then in terms of interns, with declining university numbers we’re hearing about some stiff competition for top talent for internship or graduate programmes in fields like trading and law. We’ve actually received client feedback that accommodation standards are increasingly a deciding factor for students choosing their internship, so firms are keen to enhance intern experiences.

We’re seeing some unusually high nightly budgets and requests for more premium intern accommodation in locations like London, as firms know they’ll see the long-term return on investment in terms of talent returning to their business full time, interns recommending their firm to other talent, and generally boosting the firm’s reputation as a great place to work.

This paints a different picture to how many organisations are approaching their intern programmes in the US where lump sums and stipend packages (very much a cost containment, ‘leave the guest to it’ approach) are dominating.

Global Regulatory & Policy Shifts to Be Aware Of

UK visitor levy confirmed

We mentioned them as part of our 2025 Autumn Budget review in December’s Update, but the UK government has now committed to “press ahead” with plans to allow city mayors in England to introduce visitor levies on overnight accommodation. To the dismay of many across business travel and hospitality, the Overnight Visitor Levy Bill has been confirmed for 13 authorities including London, Manchester and Liverpool.

This is at odds with other moves to make doing business in key hubs like London more attractive, so businesses might start to tighten housing budgets once more to offset higher tax burdens.

2030 EPC deadline approaching for landlords

Minimum Energy Efficiency Standards (MEES) in England and Wales now mean all privately rented commercial properties must have an EPC rating of at least C by 2030. It’s owners of older buildings who have far further to go to retrofit their properties for energy efficiency. For those unable to justify the investment, the only option will be to sell, so we might start to see large, franchise brands acquiring those buildings from private owners or a constricted supply if that stock exits the market altogether.

Brand consolidation continues

Our Chief Supply Officer predicted more brand consolidation in our 2026 trend forecast, so while the EPC mandates could add to that shift in the UK, it’s already happening worldwide. Aligning with wider mergers and acquisitions (M&A) predictions that 2026 is set to be the most valuable M&A year in history, recent industry merger announcements include:

- Equity Residential and AvalonBay will merge to become $52 billion REIT – as a merged entity, they will represent massive market share in key US locations like New York, Denver, NorCal and SoCal, Austin and Dallas, and Boston. It’s a deal that will have a huge influence on the US multifamily market and corporate buyers, so we will watch to see what changes when the merger completes.

- Technology-focused private equity company, Long Lake, will acquire corporate travel platform, Amex GBT – this will privatise Amex GBT and likely shift investment priorities towards tech, automation and AI. Perhaps a less human approach to travel management and certainly a greater pressure on accommodation providers to have strong integration and connectivity capabilities ahead.

US immigration processing delays add pressure to mobility management

Immigration policies have been changing regularly in the US and there continues to be significant delays across the US immigration system, adding more pressure to mobility programmes than ever before:

- Processing timeframes are so unreliable that paying for premium processing is no longer just an allowance for genuinely urgent requirements, but now it’s often the only way to protect against delays. Mobility teams should anticipate premium processing costs and build it into budgets as standard to avoid further overspend signoff delays.

- Assignees stuck in visa renewal processing queues are then unable to renew other documents like their driver’s licence that depend on immigration status for approval. Without a driver’s license many assignees are unable to travel for work or personal life, so mobility and HR teams should consider and support the full impact of delays beyond just the application or renewal process.

- The ending of automatic extensions for pending Employment Authorization Document (EAD) renewals, which was announced in October 2025, is continuing to cause issues for many foreign nationals working in the US. Employees were previously authorised to continue working for up to 540 days while they waited for their EAD renewal to be processed, but this is no longer the case.

The risk is that certain visa holders will be unable to work while they wait for their EAD renewal, a risk that’s far greater with the current processing delays. Try to file for renewals at least six months before the expiry date and remember to monitor the risk for spouses of visa holders as well as the employee themselves. - The US government recently proposed a new prevailing wage rule whereby companies must pay H-1B workers a higher minimum salary, which could increase wages by 17% per employee. Not only would this be a significant extra cost pressure for organisations to front but also raises concerns about fair pay and discrimination against US workers on lower salaries for similar roles.

This proposed change might be the push businesses need to review their H-1B visa cohort and start planning: if this wage rule materialises, is your business able or willing to absorb these huge additional expenses? What would be the contingency for those workers if you need to cut back on H-1B sponsorships? Can they be relocated elsewhere, and are you prepared to organise those moves?

There are a number of other challenges impacting travel, mobility and HR teams in a complex US immigration environment, so the core upshot for businesses is to get ahead of immigration risk and ensure it’s a proactive consideration in your mobility programme.

Want to Dig into More Detail?

SilverDoor's Market Update is a comprehensive review of the global travel landscape. It uses SilverDoor booking data, the experiences of our people, and wider industry, economic and geopolitical context to build a picture of worldwide business travel, mobility and corporate accommodation trends.

The data in this report is from SilverDoor’s own booking data based on a 1st February – 30th April (2025 vs 2026) reporting period. For the period of 1st February – 30th April 2026 alone, we recorded 568,000 room nights for 9,582 enquiries in 101 countries and 1,161 cities.

You can talk to us about any of the insights featured in this report; our experts are always on hand to provide impartial advice about how market trends might impact your specific operations and how to build strategic changes into your programme.

Connect with us on LinkedIn to keep up with SilverDoor news, learn more industry insights and discuss market trends. If you would like specific topics or trends to be discussed in a future SilverDoor Market Update, get in touch with us at [email protected].